Pradhan Mantri Suraksha Bima Yojana (PMSBY)

Info reference: jansuraksha.gov.in

PMSBY – A quick look

- This is a social security scheme launched by the government.

- It is a one year accidental death and disability cover.

- Under PMSBY, the risk coverage available is Rs 2 lakh for accidental death and permanent total disability, and Rs 1 lakh for permanent partial disability.

- The premium payable is Rs 12 yearly.

- The cover period starts June 1 and is up to May 31 of subsequent year.

- The cover needs to be renewed in the subsequent year, which is done through auto debit instructions.

- All bank account holders in the age group of 17 to 80 can enrol into the scheme.

- This can be done through the bank where they hold an account.

What is PMSBY?

PMSBY is a social security scheme, an accident insurance covering accidental death and disability. It is not a medical cover and will not cover the medical expenses incurred in an accident. On enrolment into the scheme, one needs to pay an annual premium of Rs 12. The cover offered by the scheme is Rs 2 Lakhs in case of accidental death or permanent total disability. In case of permanent partial disability, the cover is Rs 1 lakh.

Permanent total disability is defined as total and irrecoverable loss of both eyes or loss of use of both hands or feet or loss of an eyesight and loss of use of a hand or a foot. Permanent partial disability is defined as total and irrecoverable loss of an eyesight or loss of use of a hand or foot.

Who is eligible?

Any bank account holder (both single and joint account holders) in the age group of 17 to 80 can enrol into the scheme. In case of joint account holder, both the account holders can enrol into the scheme. In case one has multiple accounts with same or other banks one is eligible to join the scheme through one account only. Even if premium is paid through multiple accounts, only one claim will be payable per person

How does one enrol into the scheme?

The scheme is offered by general insurance companies in collaboration with the banks. One can enrol into the scheme through net banking. Alternately you can download a form from the link https://jansuraksha.gov.in/Files/PMSBY/English/ApplicationForm.pdf and submit it to the bank.

Policy certificates will not be issued to individuals as the bank is master policy holder.

What is covered and what is not included?

Death or disability as defined earlier, due to accident or natural calamity is covered under the scheme. One needs to note Suicide is not covered. Permanent partial disability without irrecoverable loss of an eyesight or loss of use of a hand or foot is not covered under the scheme.

Termination of the policy

The accident cover for the member will terminate on any of the following events and no benefit will be payable.

- Insurance cover will be terminated on attaining age 70 years subject to annual renewal up to that date

- In case of closure of Bank account

- If the member is not maintaining enough balance to keep the insurance in force, the cover will be cancelled.

- In case a beneficiary is covered under more than one premium by the Insurance Company inadvertently, insurance cover will be restricted to any one of the premium and remaining premium shall be liable to be forfeited.

Documents required for claiming

In case of an accident like a road accident or rail accident, or drowning or similar, one needs to file a police complaint and the complaint will be documentary proof required to be submitted during claim. However, in case of snake bite or fall from tree hospital medical records need to be submitted for the claim. The following documents need to furnished to corresponding bank in order to claim.

In case of Death of insured

- Original FIR or Panchnama in case of death of insured

- Post Mortem Report

- Death Certificate

In case of permanent disablement

- Original FIR/ Panchnama

- Disability Certificate issued by a Civil Surgeon

- Discharge certificate

Procedure of claim

- Contact the bank where the policy was taken

- Submit duly completed PMSBY claim form along with required documents mentioned above

- Claim form need to be submitted within 30 days from date of occurrence of the accident by claimant or nominee

- Once the form is verified by the bank for nomination, auto debit etc., it will be submitted to the insurance company within 30 days from the receipt of the form

- The insurance company will process the form within 30 days from the receipt of form from the bank

- The admissible amount will be credited to the claimant/nominee account

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

Info reference: jansuraksha.gov.in

PMJJBY – A quick look

- This is a social security scheme launched by the government

- It is a one year life cover payable on death of the insured

- Under PMJJBY, the risk coverage available is Rs 2 lakh in case of death of the insured

- The premium payable is Rs 330 yearly

- The cover period starts June 1 and is up to May 31 of subsequent year

- The cover needs to be renewed in the subsequent year, which is done through auto debit instructions

- Bank account holders in the age group of 18 to 50 can enrol into the scheme

- The life cover is upto age 55 only

- This can be done through the bank where they hold an account

- The cover under PMJJBY is for death only and hence benefit will accrue only to the nominee

- PMJJBY is a pure term insurance policy, which covers only mortality with no investment component

- The premium remains same for all ages

- Tax benefit is available for the premium paid under section 80C

What is PMJJBY?

PMJJBY is a social security scheme, a life insurance covering loss of life. On enrolment into the scheme one needs to pay an annual premium of Rs 330. The cover offered by the scheme is Rs 2 Lakhs in case of death of the insured. Life cover is valid upto age 55.

Who is eligible?

Any bank account holder (both single and joint account holders) in the age group of 18 to 50 can enrol into the scheme. In case of joint account holder, both the account holders can enrol into the scheme. In case one has multiple accounts with same or other banks one is eligible to join the scheme through one account only. Even if premium is paid through multiple accounts only one claim will be payable per person.

Insurance buyers joining the scheme after the primary enrolment period ranging from 31st Aug – 30th Nov 2015 will have to submit a self-attested medical certificate as a proof that he/she is not suffering from any critical illness mentioned in the policy declaration form.

How does one enrol into the scheme?

The scheme is offered by life insurance companies in collaboration with the banks. One can enrol into the scheme through net banking. Alternately you can download a form from the link https://www.jansuraksha.gov.in/Forms-PMJJBY.aspx and submit it to the bank.

Policy certificates will not be issued to individuals as the bank is master policy holder.

What is covered and what is not included?

Risk cover under PMJJBY is applicable only after the first 45 days of enrolment. In other words, insurers do not have to settle claims during the first 45 days from the date of enrolment. However, deaths due to accidents will be exempt from the lien clause and will still be paid.

Termination of the policy

The life cover for the member will terminate on any of the following events and no benefit will be payable.

- Insurance cover will be terminated on attaining age 55 years subject to annual renewal upto that date (entry however is not possible beyond age 50)

- In case of closure of Bank account

- If the member is not maintaining enough balance to keep the insurance in force, the cover will be cancelled

- In case a beneficiary is covered under more than one premium by the Insurance Company inadvertently, insurance cover will be restricted to any one of the premium and remaining premium shall be liable to be forfeited

Can individuals who leave the scheme re-join?

Individuals who exit the scheme at any point may re-join the scheme in future years by paying the annual premium. However, for such subscribers, insurance benefit shall not be available for death (due to any cause other than accident) occurring during the first 45 days from the date of enrolment into the scheme.

What is covered and what is not included?

Death due to any reason is covered under the scheme. This includes Suicide. Since this is a pure term insurance there is no maturity benefit applicable if the insured survives age 55.

Steps to be taken by the Nominee

- Nominee to approach the Bank wherein the Member was having the ‘Savings Bank Account’ through which he/she was covered under PMJJBY, along with the death certificate of the member

- Nominee to collect Claim Form, and Discharge receipt, from the Bank or any other designated source like insurance company branches, hospitals, PHCs, BCs, insurance agents etc., including from designated websites.

- Nominee to submit duly completed Claim Form, Discharge Receipt, death certificate along with photocopy of the cancelled cheque of the nominee’s bank account (if available) or the bank account details, to the Bank wherein the Member was having the ‘Savings Bank Account’ through which he/she was covered under PMJJBY

Link to claim form https://www.jansuraksha.gov.in/Files/PMJJBY/English/ClaimForm.pdf

Steps to be taken by the bank

- Upon receipt of death intimation, the Bank should check whether the cover for the said member was in-force on the date of his death, i.e., whether the premium for the said cover on Annual Renewal Date, i.e. 1 st of June, prior to the Member’s death was deducted and remitted to the Insurance Company concerned

- Bank to verify the Claim Form & the nominee details from the records available with them and to fill in the relevant columns of the Claim form

- Bank to submit the following documents to the designated office of the Insurance Company concerned: a. Claim Form duly completed b. Death certificate c. Discharge Receipt d. Photocopy of cancelled cheque of the Nominee (if available)

- Maximum time limit for Bank to forward duly completed claim form to Insurance Company is thirty days from the submission of the claim to it

Steps to be taken by the insurance company

- Verify that the Claim form is complete in all respects and all the relevant documents have been attached. If not, take up with the Bank concerned

- If the claim is admissible, the designated office of the insurer shall check whether the member’s coverage is in force and no death claim settlement has been made for the Member through any other account. In case any claim has been settled, then the Nominee shall be intimated accordingly with a copy marked to the Bank

- In case the coverage was in force and no claim has been settled for the said member, payment shall be released to the Nominee’s bank account and a communication shall be sent to the nominee with copy marked to the Bank

- Maximum time limit for Insurance Company to approve claim and disburse money is thirty days from the receipt of the claim from the bank

Sukanya Samruddhi Yojana (SSY)

Info reference: sukanyasamriddhiaccountyojana.in

SSY – A quick look

- Sukanya Samriddhi Yojana is a small deposit scheme of the Government of India meant exclusively for a girl child and is launched as a part of Beti Bachao Beti Padhao Campaign

- The scheme is meant to meet the education and marriage expenses of a girl child

- It has long maturity period (21 years form the date of opening)

- The interest rate for Sukanya Yojana for the current year 2019-20 is set to be 8.4% compounded yearly

- This rate of interest is however not permanent and would keep changing every fiscal year based on the economic factors.

- This happens to be the best interest rate among other saving schemes including PPF

- High interest rate coupled with EEE status and tax exemption available under section 80C for investments in SSY makes this scheme very popular

Eligibility

Eligibility

- Account can be opened by the parent or legal guardian in the name of the girl child who is less than 10 years of age

- Maximum of 2 accounts, one per girl child, can be opened by the parent, unless the second is a twin or the first is a triplet, in which case, 3 accounts are allowed

- Multiple accounts cannot be opened in the name of one girl child

Where can one open the account?

- The account can be opened in a post office or scheduled commercial banks which are authorized to open this account

- The account may be transferred anywhere in India, if the a/c holder shifts

- This link gives you a list of banks where the account can be opened https://www.sukanyasamriddhiaccountyojana.in/list-of-authorized-banks-for-ssa-ssy/

What are the documents required for opening an account?

- Birth Certificate of the girl child

- Address proof of the guardian

- Identity proof of the guardian

Maximum and Minimum Deposits

- The minimum deposit to be made per year is INR 250 and maximum deposit is INR 150000 per year, per account

- While the account can be opened with a minimum deposit of INR 250, subsequent to opening the account, one can deposit in multiples of hundred, subject to the above-mentioned limits per year

- Deposits can be made in lump-sum or periodically. There is no limit on the number of deposits either in a month or in a financial year

- If the minimum amount of INR 250 has not been deposited, then such an account can be regularized by paying penalty of INR 50 per year along with a minimum deposit INR 250 per year of default any time till the account completes fourteen years

- If the penalty is not paid, the entire deposit, including those made before the date of default, will receive interest at post office savings bank account rate, which is currently 4%. If excess interest has been paid, it will be reversed

Time period of the Account

- The deposits are to be made for minimum 14 years from the date of opening the account.

- The account will mature on completion 21 years from the date of opening the account or on marriage of the girl after she attains 18 years of age.

- If the girl were to get married after attaining 18 years of age the account will be prematurely closed and the maturity proceeds will be paid. According to the new norms, no such premature closure shall be allowed before one month of the date of the marriage or after three months from marriage

- The Sukanya Samriddhi account will mature on completion of a period of twenty-one years from the date of its opening. No interest shall be payable once the account completes twenty-one years from the date of opening

Rate of Interest

- Rate of Interest for this scheme is not fixed. The interest is subject to revision every financial year. For this year (FY20) the interest payable will be 8.4%.

- Interest will be compounded on a yearly basis

- Interest will be paid on the balance to the nearest thousand (downwards) in the account. Eg. If the balance is INR 50,784, Interest will be paid on INR 50,000.

Tax treatment

- The deposits are eligible for deduction under section 80C

- The taxation status is EEE. This means that the deposits are exempt from tax, the interest earned is exempt and the maturity amount is exempt as well

Premature withdrawal

- Now, partial withdrawal up to 50 per cent of the account balance will be allowed for the purpose of higher education of the account holder (the girl child) if she attains the age of eighteen years or has passed the tenth standard, whichever is earlier

- However, for the partial withdrawal, documentary proof in the form of offer of admission of the account holder in an educational institution or a fee-slip from such institution has to be submitted

- The partial withdrawal will be made as one lumpsum or in instalments, not exceeding one per year, for a maximum of five years

- If the educational fee is less than 50 per cent of the account balance, the partial withdrawal amount will be restricted only to the fee amount

Premature closure

- On death of the account holder, the account will be closed immediately on production of death certificate.

- Interest will be payable till the last completed month prior to the premature closure.

- The balance in the account shall be paid to the guardian of the account holder

- In cases of extreme compassionate grounds such as medical support in life-threatening diseases, death etc., the account can be closed prematurely

Drawbacks of the scheme

- The withdrawal and premature closure norms are extremely stringent, as it doesn’t even allow complete withdrawal for higher education. It is primarily aimed to fund the marriage expenses. If this is not your intent, it would be ok to skip this.

- While recommending this to economically backward section, one needs to remember their reluctance to deal with cumbersome withdrawal and closure procedures. Even for marriage the amount is available only a month before the date of marriage

Pradhan Mantri Awas Yojana (PMAY)

Info reference: pmaymis.gov.in, various bank websites

PMAY – A quick look

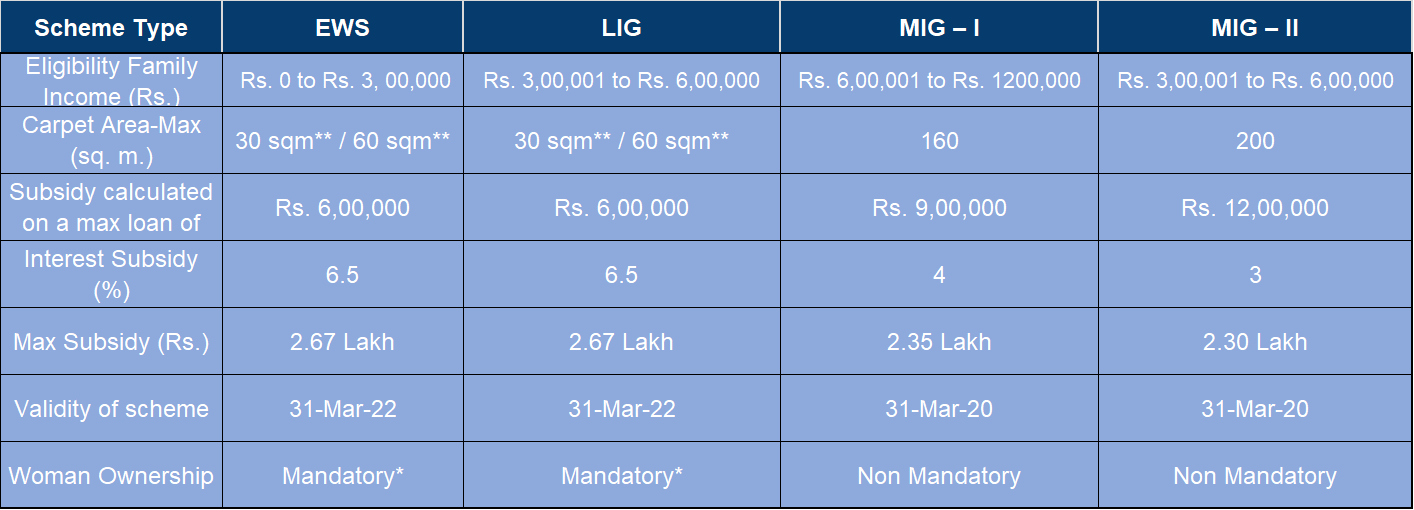

- Pradhan Mantri Awas Yojana was launched with the aim to provide housing at an affordable price to the weaker sections of the society, lower income group people, urban poor, and rural poor

- Through the Credit Linked Subsidy Scheme (CLSS) under PMAY, subsidy is given on interest payable on home loans

- This makes the home loan affordable as the subsidy provided on the interest component reduces the outflow of the customer on the home loan

- The subsidy amount under the scheme largely depends on the category of income that a customer belongs to and the size of the property unit being financed

- To be eligible for the scheme, the beneficiary family should not own a pucca house in his/her or in the name of any member of his/her family in any part of India and should not have availed of any central assistance under any housing scheme from Government of India or any benefit under any scheme in PMAY

PMAY Eligibility

- The beneficiary family should not own a pucca house in his/her or in the name of any member of his/her family in any part of India.

- In case of married couple, either of the spouse or both together in joint ownership will be eligible for a single subsidy.

- The beneficiary family should not have availed of central assistance under any housing scheme from Government of India or any benefit under any scheme in

PMAY

Beneficiary Details

- The beneficiary family will comprise husband, wife and unmarried children (An adult earning member irrespective of marital status can be treated as a separate household in MIG category)

- Woman ownership is not mandatory for construction / extension in MIG category

- As per amendment dated 15.03.2018, an adult earning member (irrespective of marital status) can be treated as a separate household. Provided also that in case of a married couple, either of spouses or both together in joint ownership will be eligible for a single house, subject to income eligibility of the household under the scheme

Other relevant features

- Aadhar number(s) of the beneficiary family are mandatory for MIG category

- The interest subsidy will be available for a maximum loan tenure of 20 yrs or the loan tenure whichever is lower

- The interest subsidy will be credited upfront to the loan account of beneficiaries through bank, resulting in reduced effective housing loan and Equated Monthly Installment (EMI)

- The Net Present Value (NPV) of the interest subsidy will be calculated at a discount rate of 9%

- The additional loan beyond the specified limits, if any to be at non-subsidized rate

- There is no cap on the loan amount or the cost of the property

How can one avail of the Credit-Linked Subsidy Scheme?

- The bank where you have applied for loan will guide and help you apply for CLSS

- After the loan is disbursed, the bank will claim subsidy for eligible borrowers from National Housing Bank (NHB)

- NHB after due diligence would approve & credit the subsidy amount to the bank/ for all eligible borrowers

- On receipt of subsidy amount from NHB, same is credited to respective home loan account of the borrower and EMI is reduced proportionately

There are no additional documents except a self-declaration of not owning a pucca house in the format provided by your bank disbursing the loan